In a Flash

Recent regulations affecting

retirement planning

June 2012, Issue 2

- Podcast: The role of longevity annuities in retirement planning

- Viewpoint: What fee disclosure regulation means for plan sponsors

- Research: Effects of fees on a participant's savings

- Announcement: Connect with Financial Engines through new social media tools

PODCAST

The role of longevity annuities in retirement planning

Dr. Jason Scott, Managing Director of Financial Engines' Retiree Research Center, discusses the role of longevity annuities in retirement planning, including the impact of recently proposed regulations.

For more information, click on the additional resources below:

- The Longevity Annuity: An Annuity for Everyone

- Financial Engines comments on IRS REG-115809-11 and IRS REG-110980-10

- Dr. Scott's testimony on proposed regulations

- More information about the proposed regulations is available at irs.gov

VIEWPOINT

What fee disclosure regulation means for plan sponsors

Background

After a thorough review, the U.S. Department of Labor (DOL) has issued new rules governing fee disclosure requirements to assist both plan sponsors and plan participants. The rules are aimed at making it easier for sponsors and their employees to understand the true cost of employer retirement plans, thereby helping investors make better decisions regarding their participation in these plans.

The new rules include specific requirements that are expected to help both plan fiduciaries, when selecting and monitoring plan service providers, and individual workers, when making investment choices and evaluating fees versus returns. Here's an overview of the two major ERISA fee disclosure rules and how they affect plan sponsors.

| Section 408b-2—Service Provider Disclosure Compliance date: July 1, 2012 |

Section 404a-5—Participant Disclosure Compliance date: August 30, 2012 |

| Covers the total fees paid from the plan to service providers. Fee disclosure produced and delivered by the service providers to the plan sponsor. | Covers the total fees paid by each plan participant. Fee disclosure (in dollars) typically produced and delivered by the service providers to the plan participants via their quarterly account statements. |

What effect will these new rules have on retirement plans?

Section 408b-2—Service Provider Disclosure

ERISA Rule 408b-2—effective July 1, 2012, for both existing and new contracts or arrangements— outlines the disclosure obligations between "covered service providers" and covered 401(k) plans. The rule requires that covered service providers provide the following to the plan:

- information on the services it provides;

- its status as a fiduciary or registered investment adviser; and

- a description of the compensation (direct and indirect) that it expects to receive in connection with the services.

Previously, a provider that offered multiple services was not required to show the full cost per service. Instead, they could simply show the total investment expense; provide a fee schedule; or even fail to fully disclose all the fees. The new rule now requires service providers to disclose the total cost—both direct and indirect—of services to the plan sponsor. It also requires that service providers break out the total costs per service, including (but not limited to) record-keeping costs, administration costs, investment management costs, indirect compensation costs, and shareholder-type costs.

Because the rule will help clarify the undisclosed charges being assessed to a plan, it's expected to reduce the time and cost commitments a sponsor needs to fulfill their fiduciary duty. More specifics about this rule can be found here and here.

Section 404a-5—Participant Disclosure

From a consumer perspective, the more important rule—ERISA Rule 404a-5—requires that plan administrators provide detailed information to participants about the investment options, fees, and expenses paid by both participants and the plan for their plan investments and administration. To comply with the rule, a participant's quarterly costs should be listed clearly on the participant's quarterly account statement. This new requirement applies to plan years beginning on or after November 2, 2011, and plan sponsors must provide the disclosures by August 30, 2012.

Required participant-level disclosures are divided into two broad categories:

- Plan-related information, which includes three subcategories: general plan information (e.g., information about the structure and mechanics of the plan); administration expenses information (e.g., record-keeping or legal fees); and individual expenses information (e.g., fees for plan loans or for processing qualified domestic relations orders). According to the DOL, this information must be given to participants on or before the date they can first direct their investments, and then on an annual basis. In addition, providers must send quarterly (at least) statements to participants that outline plan-related fees and expenses deducted from the participant's individual accounts.

- Investment-related information, which refers to performance data. This information includes average total return and operating expenses, as well as the name of each designated investment alternative and the type or category of the investment. Plan administrators are also required to identify any designated investment managers for the plan.

Rule 404a-5 places responsibility for providing the required disclosures on the plan sponsor. However, plan sponsors will likely rely on plan service providers or investment product providers for the information needed to comply with the rule. More specifics about this rule can be found here.

How should plan sponsors prepare for these upcoming fee disclosure rules?

Financial Engines recommends that plan sponsors confirm with all service providers how their current compensation is structured (e.g., indirect compensation, flat fee arrangement, asset-based fee arrangement, etc.). Plan sponsors should also request an updated fee disclosure from all service providers.

Additionally, the new fee disclosure rules can help plan sponsors determine if the total costs associated with their retirement plan(s) are appropriate and/or fair in comparison to similar retirement plans, assuming this information is available through the plan provider(s). If not, then a benchmarking service or request for proposal may be necessary.

Finally, plan sponsors should establish the roles and responsibilities of all their retirement plan service providers, including defining what and how each party is being compensated. Doing so should help provide an explanation of the retirement plan cost(s) referenced in Rule 404a-5. Remember, when acting as a retirement plan fiduciary plan sponsors are responsible for understanding how much their participants are paying for each service, who is being compensated, and if the charges are reasonable.

What Financial Engines is doing to help

Financial Engines has always notified plan sponsors of their fees within their financial services agreements, and therefore has always made available the fee disclosures soon to be required. But now we are going a step further. As a covered service provider under Rule 408b-2, Financial Engines will provide plan sponsors with a separate document outlining the fees we expect to receive in connection with our services, as well as all other applicable service provider disclosures. Additionally, we will disclose our role as a "designated investment manager" under Rule 404a-5, in an effort to aid plan sponsors in their participant fee disclosures.

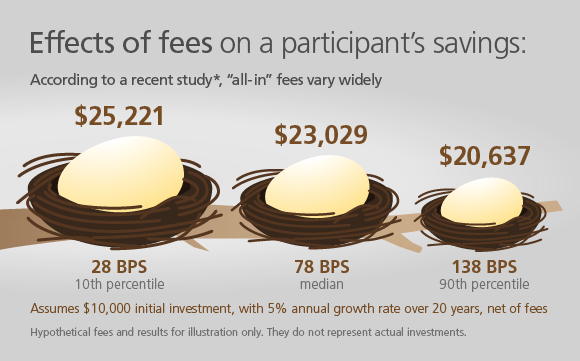

Research

*Inside the Structure of Defined Contribution/401(k) Plan Fees: A Study Assessing the Mechanics of the 'All-In' Fee. Deloitte Consulting LLP, November 2011. "All-in" fees defined as all administrative, recordkeeping, or investment fees assessed at plan, employer, or participant level. Study found participants and plan pay, on average, 95% of all-in fees, which is reflected in the hypothetical results above.

**Financial Engines and Aon Hewitt, "Help in Defined Contribution Plans: 2006 Through 2010," September 2011.

See full report.

Announcement

Connect with Financial Engines' new retirement

planning resources

To better help investors retire with confidence, Financial Engines recently launched RetireWell, our new blog that offers free education and retirement tips. We encourage you to link to RetireWell and our other retirement resources—including Twitter, YouTube, and LinkedIn—from your company intranet.| Click on the buttons below to get connected with Financial Engines. |

|||

|

|

|

|